AmCham Members & Business Media Meeting

30 Jun 2026, 11:38

This article analyses the general procedure for the refund of value added tax (“VAT”) in accordance with the Code of the Republic of Kazakhstan dated 25 December 2017 No. 120-VI “On Taxes and Other Mandatory Payments to the Budget (Tax Code)” (the “Tax Code”). It describes in detail the conditions and refund procedure, as well as the specific features of thematic audits and the application of the risk management system.

Particular attention is given to the analysis of the relevant case law, and the article also provides a brief comparative analysis of the changes relating to VAT refunds set out in the Code of the Republic of Kazakhstan No. 214-VII dated 18 July 2025 “Tax Code of the Republic of Kazakhstan” (“Tax Code 2025”).

The relevance of analysing the VAT refund procedure provided for by the Tax Code is connected with the transitional provision in Article 833 of Tax Code 2025, according to which tax applications for the refund of the excess VAT amount submitted before 1 January 2026 are considered in accordance with the procedure and time limits provided for by the Tax Code.

The purpose of this article is to provide taxpayers with a practical guide to obtaining a VAT refund and challenging a refusal to refund VAT, taking into account the case law that has been formed.

The taxpayer’s advance preparation for a tax audit conducted in connection with a VAT refund is an important stage. The purpose of this stage is to assess the lawfulness of the VAT refund claim and to ensure that the taxpayer is ready for the audit.

First of all, it is necessary to determine whether the taxpayer meets the criteria established by subparagraph 2 of paragraph 2 of Article 429 of the Tax Code for a VAT refund.

A refund is possible if the following conditions are met simultaneously:

Therefore, even before filing the VAT return (in which the refund claim is stated), it is necessary to verify that the taxpayer satisfies the VAT refund conditions.

Before initiating the refund procedure, it is advisable to collect and systematise in advance the set of documents that, with a high degree of probability, will be requested by the auditing authorities.

The basic list includes:

Advance preparation of the documentation makes it possible to reduce the time needed to respond to requests from the tax authority.

The final step in preparing for the audit is the filing of the claim for the refund of the excess VAT amount. In accordance with paragraph 6 of the Rules[1], this claim is reflected in the initial, regular or liquidation VAT return.

Thus, consistent preparation for the audit, with a focus on the lawfulness of the refund and the availability of all supporting documentation, forms the basis for the successful completion of the VAT refund procedure.

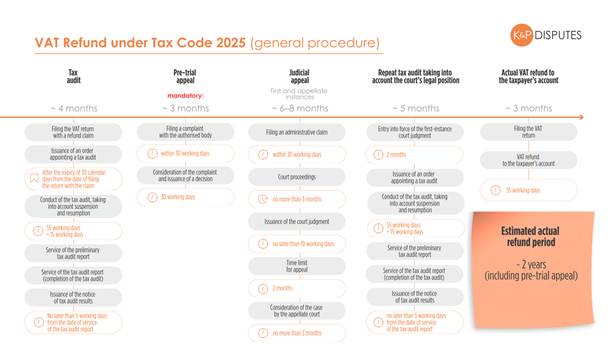

In order to confirm the accuracy of the amounts claimed for refund, a thematic tax audit is appointed (subparagraph 6 of paragraph 1 of Article 142 of the Tax Code).

The ground for conducting the audit is an order of the territorial state revenue authority, which must be checked for compliance with the requirements of paragraph 2 of Article 148 of the Tax Code. Particular attention should be paid to the correctness of the period under audit, since errors in determining it may entail procedural violations and become grounds for declaring the audit unlawful.

According to paragraph 8 of the Rules, a thematic audit is conducted using the risk management system (“RMS”), which is based on risk assessment and includes measures developed and applied by the tax authorities in order to identify and prevent risk.

Violations identified through the RMS are the main risk area for the taxpayer, since the existence of an RMS risk on the part of suppliers may serve as a ground for refusing a VAT refund (paragraphs 46-48 of the Rules).

The duration of a thematic tax audit, as well as the possible grounds and procedure for its extension or suspension, are governed by paragraph 2 of Article 431 of the Tax Code:

The tax authority is entitled to take the following actions:

In practice, the implementation of the provisions referred to in items (2) and (3) involves the time required to obtain responses to such requests, which often exceeds the statutory audit period.

In certain cases, the tax authorities send requests at a late stage of the audit. This results in the impossibility of obtaining responses within the established period, which may subsequently be used as a ground for refusing a VAT refund by reason of the absence of supporting documentation.

For this reason, it is recommended that regular and constructive communication be maintained with the inspecting officer at all stages of the audit, rather than only when formal requests are received. This increases the likelihood that the necessary requests will be sent in good time.

If requests are sent in the last days of the audit, it is necessary to insist on suspension of the audit until responses are received.

Before the final tax audit report (the “Report“) is prepared, the tax authority issues a preliminary report, in respect of which the taxpayer is entitled to submit written objections in accordance with Article 157 of the Tax Code.

The date of completion of the tax audit is deemed to be the date on which the final Report is issued (paragraph 3 of Article 158 of the Tax Code).

On the basis of subparagraph 2 of paragraph 2 of Article 114 and paragraph 1 of Article 159 of the Tax Code, the notice of the audit results (the “Notice“) must be served on the taxpayer no later than five working days after the Report is served.

As practice shows, the tax authorities often refuse VAT refunds, which requires the Notice to be challenged subsequently.

The procedure for challenging the results of a tax audit is governed by the provisions of the Tax Code and the APPC[2].

According to paragraph 31 of the Supreme Court’s Regulatory Resolution[3], based on the provisions of Article 159 of the Tax Code, the decision resulting from a tax audit is the notice of the audit results.

Accordingly, where the taxpayer disagrees with the failure to confirm the excess VAT amount for refund, only the Notice is subject to challenge.

Before bringing a judicial challenge, the taxpayer is entitled to file a complaint with the Ministry of Finance of the Republic of Kazakhstan, which is considered by the Appeals Commission. According to paragraph 1 of Article 178 of the Tax Code, such complaint may be filed within 30 working days from the date of service of the Notice.

Detailed explanations of the procedure and time limits for both judicial and pre-trial challenges are set out in our handbook “Tax Disputes: A Guide to Case Law. Part 1. Effective Application of the APPC” (KP Disputes) https://kplaw.kz/kp-education.

The practice of considering complaints shows a comparatively low rate of success. Thus, following the first quarter of 2025, the Appeals Commission under the Ministry of Finance considered 47 complaints, of which only 32% were upheld (in whole or in part) (https://www.gov.kz/memleket/entities/minfin/press/article/details/199190).

Nevertheless, despite the statistically unfavourable trend, pre-trial challenge retains practical significance. Article 15-1 of the APPC contains requirements aimed at achieving uniformity in administrative procedures, and since the case law in this category of disputes has become settled in favour of taxpayers and must be taken into account when complaints are considered, such case law increases the taxpayer’s prospects at the pre-trial stage. A complaint filed at the pre-trial stage may:

According to part 5 of Article 91 of the APPC, unless otherwise provided by law, an application to the court is permitted after a pre-trial dispute resolution procedure has been complied with.

According to paragraph 2 of Article 177 of the Tax Code, the taxpayer is entitled to challenge the notice of the tax audit results directly in court without applying to a superior authority.

Thus, the above provision of the Tax Code allows the taxpayer to apply directly to the court without prior pre-trial challenge.

Tax authorities often rely on common grounds for refusing a VAT refund (violations on the part of suppliers at subsequent levels; absence of responses to requests), while frequently disregarding both the provisions of the Tax Code and the Rules and the legal positions that have developed in the case law.

In this category of cases, a settled body of case law has already developed, which generally increases the predictability of judicial challenges.

Set out below are the most common grounds for refusing a VAT refund which most taxpayers encounter.

Violations by Suppliers at Subsequent Levels

Tax authorities interpret the Rules expansively in their own favour. When conducting thematic audits to confirm the accuracy of the excess VAT amount, they use the RMS provided for by paragraph 37 of the Rules. According to paragraph 45-1 of the Rules, the report “Pyramid” is formed for all levels of the taxpayer’s suppliers, except in the cases referred to in paragraphs 46 and 47.

The indicators of risks of tax evasion under paragraph 47 of the Rules are:

When considering VAT refund issues, the tax authorities in fact ignore the provisions of subparagraphs 2 and 3 of paragraph 12 of Article 152 of the Tax Code. As a result, refunds are often refused where the analytical report “Pyramid” reveals alleged violations on the part of the audited taxpayer’s suppliers.

As grounds for reviewing suppliers at subsequent levels, the tax authorities rely on paragraphs 45-1 and 47 of the Rules, which provide for RMS-based analysis at all supplier levels. This approach has given rise to numerous disputes because it goes beyond the wording of the Tax Code and effectively imposes stricter requirements on taxpayers.

For this reason, provisions of the Rules which worsen the taxpayer’s position as compared with the provisions of the Tax Code cannot be applied in the absence of corresponding amendments to the Tax Code itself. In disputes concerning VAT refunds, the Tax Code should therefore prevail as the higher-ranking legal act.

At the same time, a literal interpretation of the above provisions shows that, for VAT refund purposes, only violations on the part of the taxpayer’s direct supplier are legally relevant.

This position is confirmed by the case law:

“Expansive application of the provisions of tax legislation. The audit should have been limited to the claimant’s relationships with its direct suppliers, whereas the defendant analysed suppliers of the sixth level and used that analysis as a basis for refusal.”

“The service provider generates the ‘Pyramid’ report on the risk of non-performance of tax obligations exclusively in respect of the direct suppliers of the service recipient.”

The above approach has been affirmed by the Judicial Panel for Administrative Cases of the Supreme Court of the Republic of Kazakhstan (the “SCAP SC“):

“That is to say, the literal meaning of such expressions used by the legislator as ‘direct supplier’ and ‘supplier of the audited taxpayer’ leads to the conclusion that the Tax Code clearly limits the use of the analytical report ‘Pyramid’ to the direct suppliers of the audited taxpayer.”

“It follows from the literal content of the above provisions that the refund of the VAT amount is not made if violations are identified on the basis of the report ‘Pyramid’ in relation to the claimant’s direct suppliers.”

The foregoing is also confirmed by the amendments and additions made to the Rules by Order No. 137 of the Minister of Finance of the Republic of Kazakhstan dated 12 March 2024 (effective from 26 March 2024). According to paragraphs 45 and 45-1, the result of forming the report “Pyramid” is a summary table of settlements between the service recipient and suppliers at different levels for each tax period, except where the report is generated exclusively in respect of the direct suppliers of a service recipient subject to horizontal monitoring.

Thus, the case law proceeds on the basis that, for VAT refund purposes, legal significance attaches to the taxpayer’s relationships precisely with its direct suppliers.

The tax authorities send requests to banks, state authorities (including foreign authorities) and territorial state revenue authorities. However, in practice such requests are often sent only at the final stage of the audit, without the audit being suspended, as a result of which responses are not received before the audit is completed. The absence of responses by the date of completion of the audit is then used as a ground for refusing the refund.

Requests sent by the tax authorities to foreign tax authorities usually remain unanswered because of the confidentiality of the requested information and the absence of legal grounds for its disclosure.

At the same time, such requests are made despite the availability of supporting documents, which renders the sending of requests unnecessary in a number of cases.

The above conclusion is confirmed by the case law:

“In support of its disagreement with the Notice, the claimant stated that the tax audit had been carried out in breach of the statutory time limit, which resulted in the belated sending of a request to the Russian tax service and the absence of a response by the date of completion of the audit, which in turn led to the refusal to confirm the VAT amount for refund.”

Taking into account the circumstances established in the case, the court comes to the conclusion that the claim is well founded in this part.

“In this administrative case, the defendant commenced the tax audit on 04 July 2024. At the same time, requests to the Sverdlovsk Region Directorate of the Federal Tax Service and to the city of Moscow were sent only on 08 August 2024.”

Taking into account that the time limit for responding to a request is 30 days, the court considers that the defendant was obliged to send the requests immediately after the commencement of the audit.

When preparing an administrative claim, taxpayers often face ambiguity in the wording of the relief sought.

Example:

At present, the case law in relation to the relief sought has become settled:

“Analysing the evidence submitted in its entirety, the court comes to the conclusion that the claim of Rineko Group LLP for recognition as unlawful and partial annulment of the notice of the audit results, together with the obligation to issue a favourable act, is well founded in respect of VAT in the amount of KZT 90,440,194.

According to paragraph 1 of Article 156 of the APPC, if a claim challenging a burdensome administrative act affecting the rights, freedoms and lawful interests of the claimant is well founded and the court recognises the act as unlawful, the court annuls it in whole or in part.

In the event that the failure to adopt an administrative act, being the result of a refusal to issue an administrative act or of the defendant’s omission, is contrary to law or has caused a violation of the claimant’s rights, freedoms and lawful interests, the court places on the administrative body the obligation to adopt an administrative act (paragraph 1 of Article 157 of the APPC).”

“Overall, the cassation court notes that the Notice was cancelled on procedural grounds, which indicates the need for the tax authority to return to the administrative procedure and to examine the excess VAT amount claimed for refund by the claimant in strict compliance with the requirements of the law. Therefore, in this part the operative part of the judgment is subject to adjustment.”

“Where it is impossible to issue a specific decision allowing the claimant’s claims in the presence of administrative discretion, the court imposes on the defendant the obligation to adopt, taking into account the court’s legal position, the corresponding administrative act in favour of the claimant.”

<…>

“In such circumstances, it is premature for the court to determine the issue of compelling the defendant to adopt a favourable administrative act on the refund of the VAT amount in the amount of KZT 157,722,197; therefore, the claimant’s demand to impose an obligation to issue a favourable administrative act for the refund of the VAT amount in the said amount must be dismissed.”

“At the same time, taking into account that all other facts and circumstances established within the framework of the audit and reflected in the audit report initiated on the claimant’s application are not disputed, and given the absence of the need to initiate a new administrative procedure (registration of a new audit), the court, having regard to the above circumstances, considers it necessary to oblige the defendant, within one month from the date on which the judgment enters into legal force, to issue an administrative act in favour of the claimant confirming the accuracy of the amounts of value added tax on the basis of the claim of Trading and Industrial holding ‘ARAL’ LLP, taking into account the court’s legal position.”

“Nor are the arguments in the claimant’s cassation appeal concerning the unlawful refusal of the claim seeking to compel the defendant to effect a refund of the excess VAT amount well founded. According to paragraphs 2 and 18 of the Rules, the refund of the excess VAT amount is carried out at the location of the service recipient, provided that there are no tax arrears. Accordingly, the performance of this obligation could only have been imposed on the State Revenue Office for Almaty District of the Department of State Revenue for the City of Astana of the State Revenue Committee of the Ministry of Finance of the Republic of Kazakhstan, which was not joined to the present case as a defendant. Moreover, the final amount of VAT refundable to the service recipient, taking into account the court’s legal position, must be calculated by the tax authority itself.”

At the same time, the operative part of the judgment is subject to adjustment in order to exclude the need to repeat the administrative procedure by issuing and registering a new order appointing an audit.

Since the courts correctly established the circumstances of the case and correctly applied the rules of substantive and procedural law, there are no grounds for setting aside or amending the judicial acts.

Thus, since the court cannot substitute the functions of state authorities, a settled practice has developed of requiring the tax authorities to conduct a repeat audit taking into account the court’s legal position.

On the basis of the established case law, it is recommended to use the following wording of the claims:

According to part 1 of Article 173 of the APPC, upon a reasoned application the court may order immediate enforcement of the judgment where later enforcement would cause substantial harm.

Examples of grounds in support of such an application:

For this reason, it is recommended that the periods for which the refund is claimed be determined in advance in order to avoid a situation in which the claim is returned.

After the court judgment enters into legal force (or, where it is subject to immediate enforcement), the tax authority issues a new order for the conduct of a thematic audit. In this connection, there is no need to file a VAT return marked as a refund.

The repeat audit is conducted according to the same rules as the initial audit, but with mandatory regard to the legal position set out in the court judgment. This means that the tax authority has no right to rely again on grounds for refusing the VAT refund which have already been found unlawful by the court. In practice, the repeat audit must be conducted in the light of the court’s legal position and cannot be based on arguments previously rejected by the court.

The procedure and time limits for the refund of the excess VAT amount are governed by Article 431 of the Tax Code. The basis for the actual crediting of the VAT amount to the taxpayer’s current account is the audit report together with the notice confirming the accuracy of the excess VAT amounts.

Step 1: after completion of the repeat audit and receipt of the tax audit Report together with the Notice of the results of the tax audit, the taxpayer must, within five working days, file the tax application in the form approved by paragraph 16 of the VAT Refund Rules for offsetting and/or refunding taxes, budget payments, penalties, default interest and fines.

In practice, after service of the Report and the Notice following the tax audit, inspectors often recommend that the taxpayer refrain from filing the said tax application, referring to the absence of funds in the budget and assuring that they will later indicate when the application should be submitted.

From a practical perspective, it is recommended not to take the position of the tax authority into account and to file the application at the earliest opportunity.

Step 2: from the moment the said tax application is registered, the inspector prepares a refund order in two copies (paragraph 17 of the Rules), which is then sent to the State Revenue Office at the taxpayer’s place of registration and subsequently transmitted to the Treasury Department.

As a general rule, the refund period of 55 working days provided for in paragraph 2 of Article 431 of the Tax Code applies. The calculation of this period begins after the expiry of 30 calendar days from the deadline established for filing the VAT return.

Example:

If the VAT return is filed for Q2 2025, the 30-calendar-day period expires on 15 August 2025. Accordingly, the 55-working-day period begins on 16 September 2025. Taking into account the official production calendar, the deadline for the VAT refund would be 3 December 2025.

However, in practice the refund is often made late because of a shortage of budget funds.

Such refusal is justified by the tax authorities by reference to paragraph 226 of the Budget Execution Rules[6], according to which, in the event of insufficiency of funds, the state treasury authorities do not accept payment orders for the refund of overpaid taxes to taxpayers, including excess VAT.

Before Tax Code 2025 entered into force, a refusal based on insufficiency of funds in the budget was considered unfounded and did not release the tax authorities from the obligation to pay default interest for late refund. However, in accordance with the second paragraph of paragraph 10 of Article 125 of Tax Code 2025, in the event of insufficiency of funds on the control cash account provided for by the budget legislation of the Republic of Kazakhstan, default interest is not accrued on the amount of the late refund of excess VAT.

Thus, Tax Code 2025 expressly provides for the possibility of not applying default interest due to the absence of funds in the budget, which makes recovery of default interest impossible in such circumstances.

At the same time, it should be noted that, in general, the taxpayer’s right to recover default interest has not been lost: paragraph 10 of Article 125 of Tax Code 2025 preserves such possibility.

The table below sets out a comparative overview of the main changes and additions introduced by Tax Code 2025 as compared with the current Tax Code.

| Tax Code | Tax Code 2025 |

| General VAT refund procedure | |

| Article 429(2) | Article 125(2) |

| The excess VAT amount at the end of the tax period is refundable in accordance with Article 431 of the Tax Code if the following conditions are met simultaneously: the taxpayer regularly supplies goods, works and services subject to the zero rate (not less than once per quarter during 3 consecutive tax periods);the share of such turnover is at least 70% of the total taxable turnover in the relevant period. If the conditions established by Article 429(2) are not met, the excess amount of value added tax is refundable only in the part of the tax amount credited in respect of goods (works, services) used for the purposes of zero-rated supplies (Article 429(3)). | The excess VAT amount is refundable to the following taxpayers: those making supplies of goods, performing works or rendering services subject to the zero rate;those carrying on activities under a subsoil use contract;those acquiring goods, works and services in connection with the construction, under a long-term contract, of production buildings and structures first put into operation in the territory of the Republic of Kazakhstan. For taxpayers making supplies of goods, performing works or rendering services subject to the zero rate, the following are refundable: where supplies are regular – the excess tax amount;where supplies are not regular – part of the tax amount credited in respect of goods, works and services used for the purposes of zero-rated supplies. Regular supply means the supply of goods (services, works) subject to the zero rate where the following conditions are met simultaneously: the supplies are made during three consecutive tax periods;the zero-rated taxable turnover for the tax period is at least 70 per cent of the total taxable turnover from supplies. At the same time, regular supply is recognised only where such supply takes place in each of the said tax periods (Article 126(1) and (2)). |

| Article 431(3) | Article 125(3) |

| No refund of the excess VAT amount is made: to a taxpayer making settlements with the budget under the special tax regime established for: small and medium-sized businesses; peasant or farming enterprises; producers of agricultural products, aquaculture (fish-farming) products and agricultural cooperatives;to a taxpayer for tax periods in respect of which it applied Article 411 of the Tax Code. | The excess tax amount is not refundable where it is: credited on invoices issued by a procurement organisation in the agro-industrial sector;credited in respect of goods, works and services relating to minerals transferred in kind in discharge of the tax obligation;formed in tax periods in which the taxpayer credited an additional tax amount. |

| Time Limits | |

| Article 431(2) | Article 128(5) |

| The refund of the excess value added tax amount confirmed by the audit results is made to the taxpayer within the following periods: where the taxpayer carries out zero-rated supplies amounting to at least 70% of the total taxable turnover from supplies for the tax period in respect of which the claim for a refund of the excess VAT amount is made – within fifty-five working days;in other cases – within seventy-five working days. At the same time, the period for refund of the excess value added tax amount begins after the expiry of thirty calendar days from the deadline established for filing the VAT return. | The excess tax amount confirmed for refund on the basis of the results of a thematic tax audit is refundable within fifty-five working days following the expiry of the deadline for filing the tax return containing the refund claim. The excess tax amount on the basis of the conclusion to the tax audit report is refundable within ten working days following the day on which the conclusion to the tax audit report is served. |

| Grounds for Refusal of a VAT Refund | |

| Article 152(12) | Article 166(11) |

| No refund of VAT is made within the amounts in respect of which, as at the date of completion of the tax audit: responses to requests for cross-check audits to confirm the accuracy of mutual settlements with the supplier have not been received;violations have been identified in respect of the suppliers of the audited taxpayer on the basis of an analysis of the analytical report “Pyramid”;the accuracy of the value added tax amounts has not been confirmed;the accuracy of the value added tax amounts has not been confirmed owing to the impossibility of conducting a cross-check audit, including because of:the absence of the supplier at its place of location;loss of accounting documentation. | No refund of VAT is made on the basis of the results of a thematic audit where: responses to requests for cross-check audits to confirm the accuracy of mutual settlements with the supplier and purchaser have not been received, or a cross-check tax audit has not been conducted, including because of:the absence of the supplier at its place of location;loss of accounting documentation;an understatement of the amount of value added tax on goods sold, works performed and services rendered has been identified by comparing the information reflected in the VAT reporting of the direct supplier for the tax period with the information in the information system of electronic invoices for all invoices issued by the supplier;criminal proceedings have been instituted under Articles 216 and 245 of the Criminal Code involving the taxpayer in respect of whom the tax audit is being conducted, or its direct supplier;the issuance of electronic invoices has been suspended (restricted) in respect of the audited taxpayer or its direct supplier;there are VAT arrears on the part of the direct supplier;foreign currency proceeds have not been received (or have not been received in full);the fact of export of goods has not been confirmed (or has been confirmed only in part). |

| Challenge to Audit Results | |

| Article 177(2) | Article 191(1) |

| The taxpayer is entitled to challenge the notice of the audit results, as well as the notice of the results of horizontal monitoring, in court. | Judicial challenge to the notice of the tax audit results and to the actions (omissions) of officials of the tax authority is carried out in accordance with the procedure provided for by the APPC. In accordance with Article 9(3) of the APPC, an application to the court may be made after compliance with the pre-trial dispute resolution procedure, unless otherwise provided by law. |

Key Changes

One positive point is that the grounds for non-refund of VAT in paragraph 11 of Article 166 of Tax Code 2025 use the term ‘direct supplier’, which should reduce the number of disputes. Previously, the Tax Code used the term ‘supplier of the audited taxpayer’, as a result of which the tax authorities were able to interpret expansively violations by suppliers at any level for the purpose of refusing a VAT refund.

Conclusion

VAT refunds in Kazakhstan remain a multi-stage and formalised procedure, the success of which depends to a large extent on the quality of document preparation, understanding the logic of the tax audit and timely challenge to unlawful refusals.

During the transitional period associated with the entry into force of Tax Code 2025, particular importance attaches both to the established case law and to the correct determination of the applicable regulation.

We hope that this article will be useful to taxpayers as a practical reference point when seeking VAT refunds and protecting their rights.

This material does not constitute legal advice. For assistance with VAT refund procedures or challenges to refusals to refund VAT, please write to contact@kplaw.kz.

[1] Rules for the return of excess value-added tax and the application of a risk management system to confirm the accuracy of the amount of excess value-added tax, as well as risk level criteria, approved by Order of the Ministry of Finance of the Republic of Kazakhstan dated March 19, 2018, No. 391

[2] Code of the Republic of Kazakhstan No. 350-VI of June 29, 2020, “Administrative Procedure Code of the Republic of Kazakhstan”

[3] Regulatory Resolution of the Supreme Court of the Republic of Kazakhstan No. 9 of December 22, 2022, “On Certain Issues Concerning the Application of Tax Legislation by Courts”

[4] Code of the Republic of Kazakhstan No. 377-V dated October 31, 2015, “Civil Procedure Code of the Republic of Kazakhstan”

[5] Regulatory Resolution of the Supreme Court of the Republic of Kazakhstan No. 5 dated November 29, 2024, “On Judicial Decisions in Administrative Cases”

[6] Rules for the Execution of the Budget and Cash Management for the 2025 Fiscal Year, approved by Order No. 272 of the Ministry of Finance of the Republic of Kazakhstan dated June 9, 2025